About

South Korea's public export finance agencies—currently among the world's largest supporters of fossil fuel infrastructure—face a strategic choice. Between 2020 and 2024, they committed KRW 61.3 trillion to overseas energy projects, with fossil fuels accounting for 74.5%.

This report provides the first quantitative assessment of how realigning with the global clean energy transition would reshape economic outcomes for South Korea. Using a newly compiled database of overseas energy projects and comprehensive value-chain analysis, it reveals a counterintuitive finding: transitioning from fossil fuel to clean energy financing could more than double jobs by 2035 while significantly increasing GDP contribution.

The analysis covers the complete value chains of both fossil fuel projects (oil and gas production, transportation, refining, petrochemicals, power generation) and clean energy projects (solar PV, wind, energy storage systems, battery manufacturing), examining four scenarios aligned with IEA climate pathways through 2035.

Executive summary

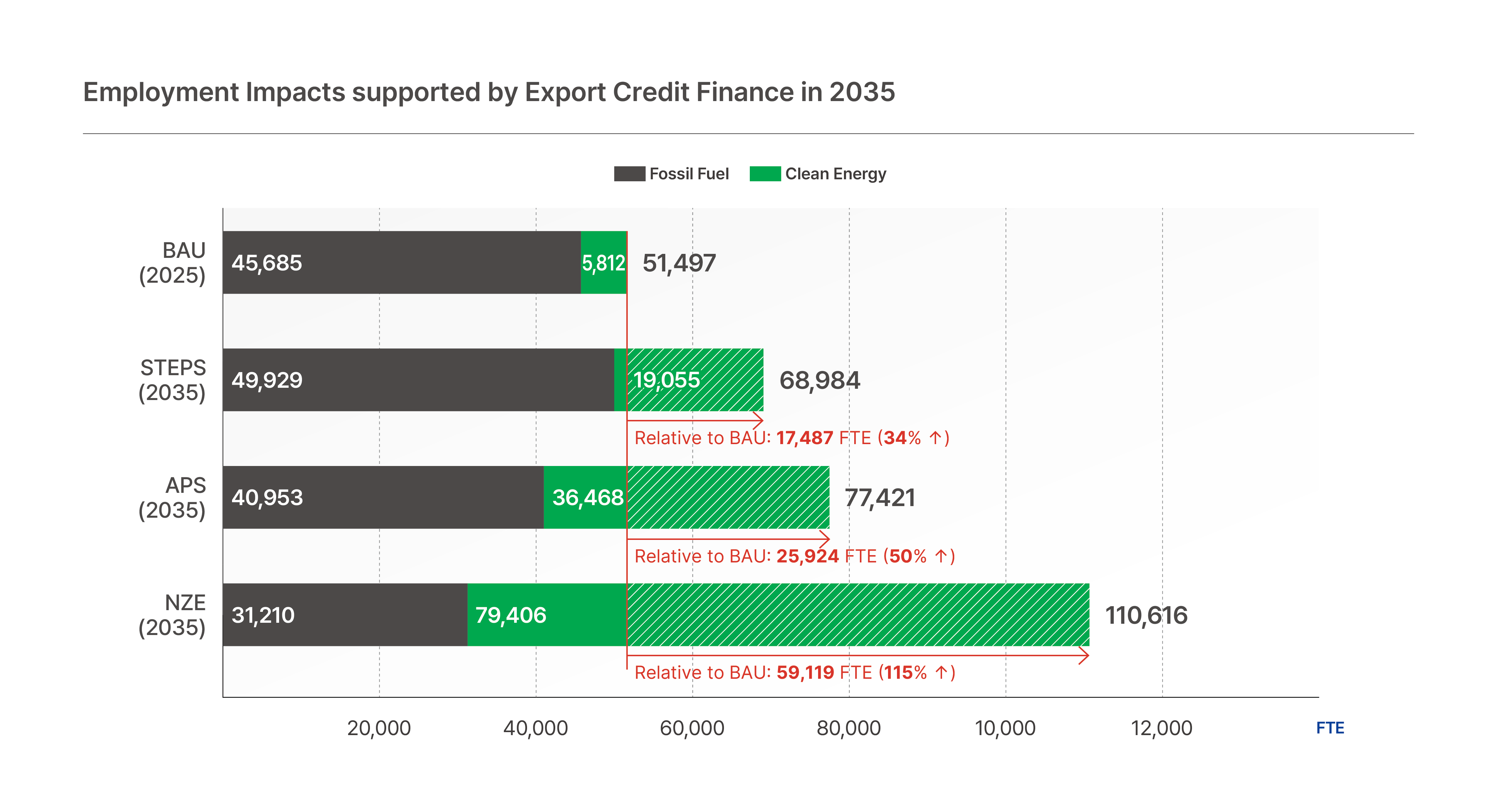

Korea's continued fossil fuel financing may actually cost jobs rather than create them. Under a Net-Zero pathway, total employment supported by public export finance reaches 110,616 full-time positions in 2035—59,119 more jobs than maintaining current fossil-dominated portfolios. Clean energy expansion contributes 73,594 additional positions across the economy, a more than tenfold increase, while fossil fuel employment declines by 14,475 positions.

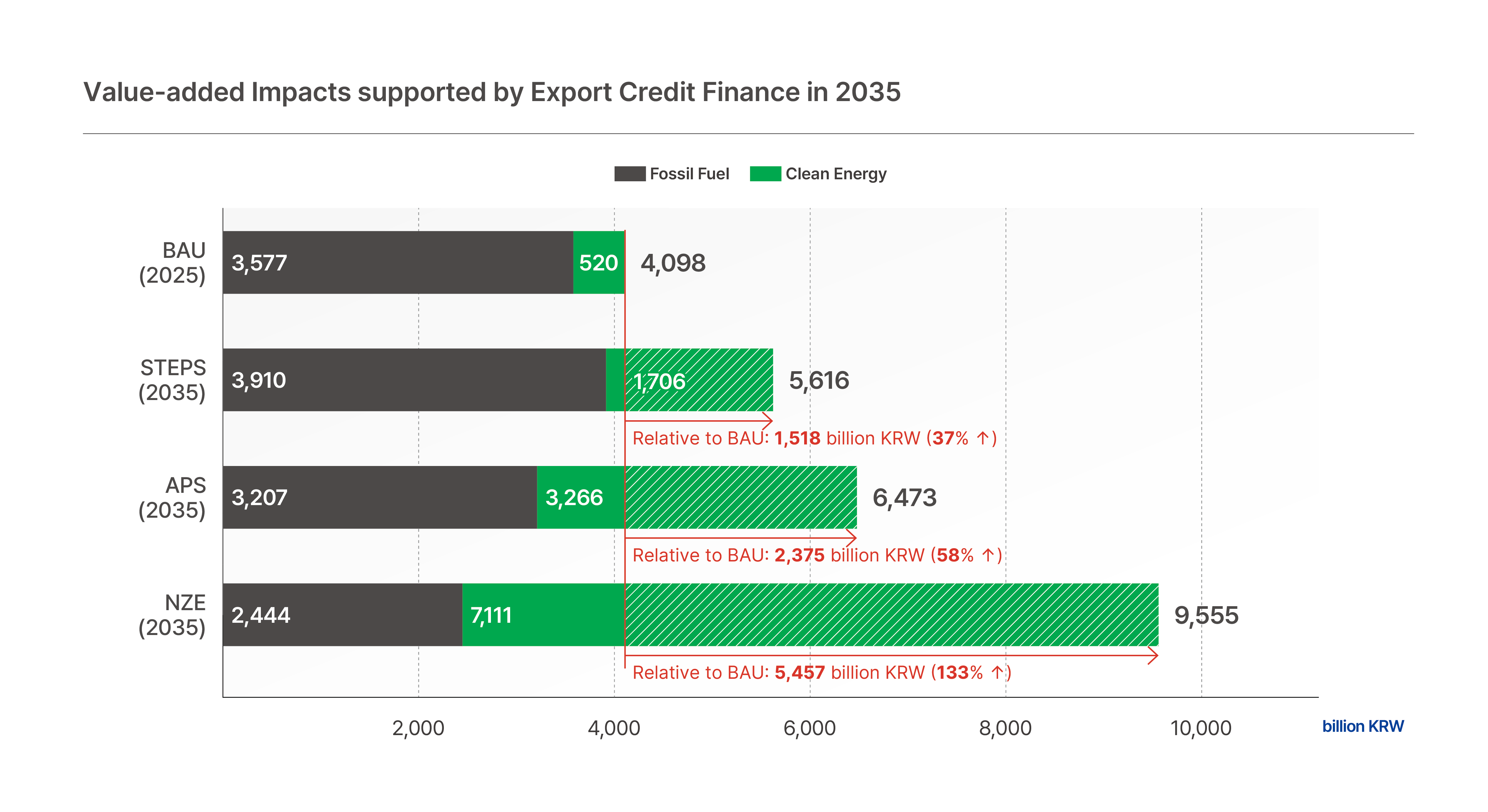

The economic case is equally compelling. Value-added contributions rise from 0.18% of 2024 GDP to 0.42% under Net-Zero scenarios, with clean energy investment adding KRW 6,591 billion in value—growing from KRW 520 billion to KRW 7,111 billion.

Yet Korea's three main export finance agencies—KEXIM, K-SURE, and KDB—have declared carbon neutrality commitments without concrete phase-out plans. Current financing patterns show natural gas (58.1%) and oil (16.3%) dominating portfolios, concentrated in Middle East and Southeast Asian markets facing heightened stranded asset risks. Clean energy support, meanwhile, focuses on battery manufacturing rather than generation infrastructure.

The transition requires strategic portfolio redirection. Initially, shifting to 100% clean energy by 2040 while maintaining current financing levels reduces unit economic impacts due to lower domestic content. However, enhanced export competitiveness and localized supply chains—similar to Korea's LNG carrier dominance built through public financing—could increase unit value-added from KRW 0.49 to 0.65 billion per billion KRW financed.

The global clean energy transition is not a threat to Korea's export economy—it's the path to doubling its economic impact.

Key findings

Portfolio composition (2020–2024):

Total energy-related public export finance: KRW 61.3 trillion

Fossil fuels: 74.5% (Natural gas 58.1%, Oil 16.3%)

Clean energy: 25.5% (Battery manufacturing 11.9%, Solar PV 6.4%, Wind 6.3%, ESS 0.9%)

Economic impacts by 2035 under Net-Zero pathway:

Employment: 110,616 FTE total—115% increase (59,119 additional jobs) vs. business-as-usual

Value-added: KRW 9.56 trillion—133% increase (KRW 5.46 trillion additional) vs. business-as-usual

GDP contribution: Rises from 0.18% to 0.42% of 2024 GDP

Clean energy jobs: Increase more than tenfold, from 5,812 to 79,406 FTE

Fossil fuel jobs: Decline by 14,475 FTE

Value chain shifts:

Battery manufacturing becomes dominant driver, rising to 51% of total value-added under Net-Zero

LNG carriers and refining/petrochemicals—currently 64% of impacts—gradually lose economic significance

Clean energy financing currently concentrated in manufacturing rather than generation assets

Geographic patterns:

Clean energy support flows to advanced economies (US, Europe)

Fossil fuel support concentrates in Middle East and Southeast Asia

Stranded asset risk highest in regions receiving continued fossil infrastructure financing

Portfolio redirection potential:

Full shift to clean energy by 2040 at current financing levels initially reduces unit impacts

With enhanced competitiveness and localized supply chains, unit value-added could rise from KRW 0.49 to 0.65 billion per billion KRW

Employment intensity could increase from 6.14 to 6.59 FTE per billion KRW financed

Policy gap:

All three agencies (KEXIM, K-SURE, KDB) committed to 2050 carbon neutrality

None has published concrete phase-out schedules for oil and gas financing

Current policies contrast with major economies aligning ECAs with climate commitments

Related research

Hidden Methane Emissions, Tangible Economic Costs_Methane Emissions from Japan’s Imported Fossil Fuel Supply Chains: Lost Fuel Value and Heatwave-Related Climate Damages

2026-08-03

Hidden Methane Emissions, Tangible Economic Costs_Methane Emissions from Korea’s Imported Fossil Fuel Supply Chains: Lost Fuel Value and Heatwave-Related Climate Damages

2026-08-03

The Undisclosed Bill: How Hyundai Motor Group is accruing a CBAM liability it has not quantified for investors

2026-07-15

Status of the National Pension Service’s Stewardship Activities and Recommendations for a Climate Stewardship Code

2026-07-06

Steel in the Portfolio: An Engagement Framework for Institutional Investors

2026-06-16

Solving the Renewable Energy Disconnect: Enabling Korea’s 100GW RE Target Through Priority Grid Connection Policy

2026-06-01

Unlocking Agrivoltaics: Extending the Temporary Non-Agricultural Use Permission Period for Farmland

2026-05-14

Stewardship Without Climate : Reforming Korea’s Stewardship Code

2026-05-13

Financing Strategies for Coal Phase-Out: Germany's Sovereign Green Bond Model and Implications for South Korea

2026-04-21

An Assessment of Environmental and Social Impacts of LNG Carriers

2026-04-06

Recurring Crisis, Delayed Transition: From Fossil Fuel Dependence to Energy Independence

2026-03-18

Empty Seats at the Climate Table : Board Oversight Gaps in Hyundai Motor Company's Climate Governance

2026-03-03

Reforming South Korea's Power Sector: Setting the Stage For the Renewable Energy Transition

2026-02-04

Government Financing for H₂-DRI Commercialization: Comparative Risk-Sharing Cases and Implications for Korea

2026-01-26

The Changing Legal Landscape for LNG Shipping Expansion

2026-01-08

Why LNG Reduction Matters: Redefining Energy Security and Unlocking Economic Gains

2025-12-08

No Budget, No Cuts: Budget and Methane Reduction Impact Analysis for Achieving 78% Low-Methane Feed Supply Target

2025-12-03

Settled in Secret: The Opaque Grid Fee System Undermining Renewable Energy PPA Expansion in South Korea

2025-12-01

From Words to Data: Bridging Hyundai’s Climate Commitments and Disclosure

2025-11-28

Supplementary Brief: South Korea's Exposure to Shipping Stranded Asset Risks

2025-10-26

No Budget, No Cuts: Agriculture’s 2030 NDC Targets at Risk

2025-09-16

VPPs: The Key to Korea's Transition to a Renewable Energy-Based Power System

2025-08-28

Transition measures: the key to a successful transition to the OSW Special Act

2025-08-26

Bridge to Nowhere: The Doomed Fate of Korea's LNG Terminals

2025-08-19

The Climate Crisis—Culprits and Liability: Contribution of South Korea’s Top Ten Emitting Corporates to Climate Loss & Damage

2025-08-10

Accelerating Renewable PPAs in South Korea: 2025 Regulatory Updates and Unresolved Challenges

2025-08-06

Speed Bumps on the Renewable Energy Highway: Minimum Generation Levels of Thermal Power Plants

2025-08-05

Driving Hydrogen-Based Steelmaking in South Korea: Focus on Hydrogen Sourcing

2025-06-25

Can the Korean Semiconductor Industry Meet its Renewable Energy Targets? Policy Recommendations

2025-06-24

No Room for More: Why LNG Carriers Are a Climate and Financial Risk

2025-05-13

Analyzing Korea’s 2035 NDC GHG Emissions Reduction Pathway through an Integrated Assessment Model

2025-04-23

Moving Away from Coal: 2025 POSCO Holdings Climate Risk

2025-03-17

A Sleeping Giant? The National Pension Service’s Missed Potential on Climate Action

2025-03-11

Stronger Together: Unlocking Community Power for Lasting Change

2025-02-04

Missing points of “South Korea’s East Sea Blue Whale Project”

2025-01-08

Socio-economic Impacts of Energy Transition in Chungcheongnam-do

2024-12-18

Bridging the Nature Finance Gap: Aligning South Korean Banks with the Global Biodiversity Framework

2024-10-27

Still Adrift: Updated assessment of the global energy transition's impact on the LNG shipbuilding industry

2024-10-14

South Korea's PPA System: Status and Opportunities for Renewable Energy Development

2024-10-10

Billions Off Course: Japan's Oil and Gas Financing Fueling the Climate Crisis

2024-09-05

Floating Doubt: The Risks of FSRUs in Expanding Methane Gas

2024-09-03

LNG運搬船: 世界のガス取引を拡大させる海上パイプライン ――影の推進者を明らかにする

2024-06-12

Three Unseen Flaws of the Boryeong Blue Hydrogen Project in South Korea

2024-05-26

Threat of Toxic Substances: Increased Particulate Matter and Health Hazards from Ammonia Co-firing

2024-05-22

![[Brief] South Korea’s international public finance continues to block a just energy transition](https://content.sfoc.tapahalab.com/images/research/RC5Kime.jpg)

[Brief] South Korea’s international public finance continues to block a just energy transition

2024-04-02

Total Turmoil: Unveiling South Korea's Stake in Mozambique's Climate and Humanitarian Crisis

2024-01-29

LNG Carriers: The Floating Pipeline Powering Global Gas Expansion - Unveiling its Hidden Enablers

2023-11-27

![[Report] The Inconsistent 'Coal-Free Pledge' of Korea's National Pension Service](https://content.sfoc.tapahalab.com/images/research/VcDPdme.jpg)

[Report] The Inconsistent 'Coal-Free Pledge' of Korea's National Pension Service

2023-06-20

High and dry:The global energy transition's looming impact on the LNG and oil shipbuilding industry

2023-05-24

Betting on a Sinking Ship: Banks Behind the Barossa Gas Field’s FPSO

2023-04-18

Unveiling Fossil Greenwashing: Hidden Emissions of Korea's Hydrogen Scheme

2022-09-13

National Development Banks and the Climate Crisis

2022-06-13

Climate Risk Management in Financial Sector and the Role of Pension Funds

2022-02-10

![[토론회] 한국형 녹색분류체계(K-Taxonomy), 무엇이 녹색경제활동인가](https://content.sfoc.tapahalab.com/images/research/bn8jdme.jpg)

[토론회] 한국형 녹색분류체계(K-Taxonomy), 무엇이 녹색경제활동인가

2021-11-23

![[이슈 브리프] 탄소포집, 이용 및 저장기술(CCUS) 현황과 문제점](https://content.sfoc.tapahalab.com/images/research/SWESdme.jpg)

[이슈 브리프] 탄소포집, 이용 및 저장기술(CCUS) 현황과 문제점

2021-11-03

KR-DE Road to 2050 : Financing Clean Energy Transition

2021-09-28

Fueling the Climate Crisis_South Korea's Public Financing for Oil and Gas

2021-08-31