Shipping rates and demand tumble amid global oversupply and clean energy competition

Calls grow for LNG shipowners and Korean shipbuilders to rethink LNG-focused order strategy as "the era of fossil fuel carriers is drawing to a close."

August 1, 2025 (SEOUL) — The liquefied natural gas (LNG) carrier market is no longer in a temporary downturn but has entered a phase of structural decline, according to new analysis. Solutions for Our Climate (SFOC) has revealed that the current volume of stranded LNG shipping assets has reached USD 10.8 billion (KRW 15 trillion), based on the latest methodology assessing the financial risks facing the ship finance industry.

Massive speculative orders placed in 2022 without long-term contracts—driven more by expectations of rising market prices than actual demand forecasts—have intensified oversupply. Around 60 LNG carriers are currently sitting idle, roughly 10% of the global LNG fleet. At an average vessel cost of USD 194.6 million (KRW 270.2 billion), these 60 ships represent a loss of USD 11.67 billion (KRW 16.2 trillion). Even accounting for their estimated scrap value of USD 318 million (KRW 441.5 billion), the realized stranded asset value still amounts to USD 11.36 billion (KRW 15.8 trillion).

This analysis applies methodology developed by Kühne Climate Center, a logistics research foundation, along with University College London's Energy Institute, to assess the financial impact that energy transition will have on the shipping industry and ship financing sector.

The surge in idle vessels and asset write-offs signals a fundamental market imbalance. While LNG carriers have long been the backbone of energy trade, the global growth rate in LNG shipments is now sharply slowing.

Freight rates, often viewed as the barometer of the shipping industry, have plummeted to below breakeven levels. The one-year time charter rate for modern tri-fuel diesel electric (TFDE) carriers has fallen to USD 20,000 per day, a year-on-year decline of over 60% and the lowest level since 2019. Even newer, more fuel-efficient two-stroke engine vessels are earning just USD 30,000 per day, putting profitability under strain. In response, early vessel retirements are accelerating. HMM recently sold four early-2000s-built LNG carriers for scrapping at USD 19.2 million each, while Hyundai LNG Shipping scrapped the 2000-built Hyundai Cosmopia at USD 580 per ton. So far this year, eight LNG carriers have already been dismantled, matching the total scrapped over the entire year of 2024.

The LNG shipping crisis stems from a structural imbalance between stagnant demand and exploding supply. In 2024, LNG trade volume growth stood at just 0.3%, a dramatic slowdown compared to the 6–8% annual increases of prior years. This sluggish volume reflects a shortage of cargoes for transport, yet ship deliveries continue to surge.

Globally, the shift to renewables and accelerating energy transitions in key markets have stunted LNG demand faster than anticipated. Still, between 2019 and 2022, amid the Russia-Ukraine war and global energy crisis, LNG ships were ordered without firm contracts—driven by speculative hopes of future price hikes. Many of these ships began entering service in late 2024, compounding the glut. At the time, this boom was misread by some as a lasting LNG shipping supercycle.

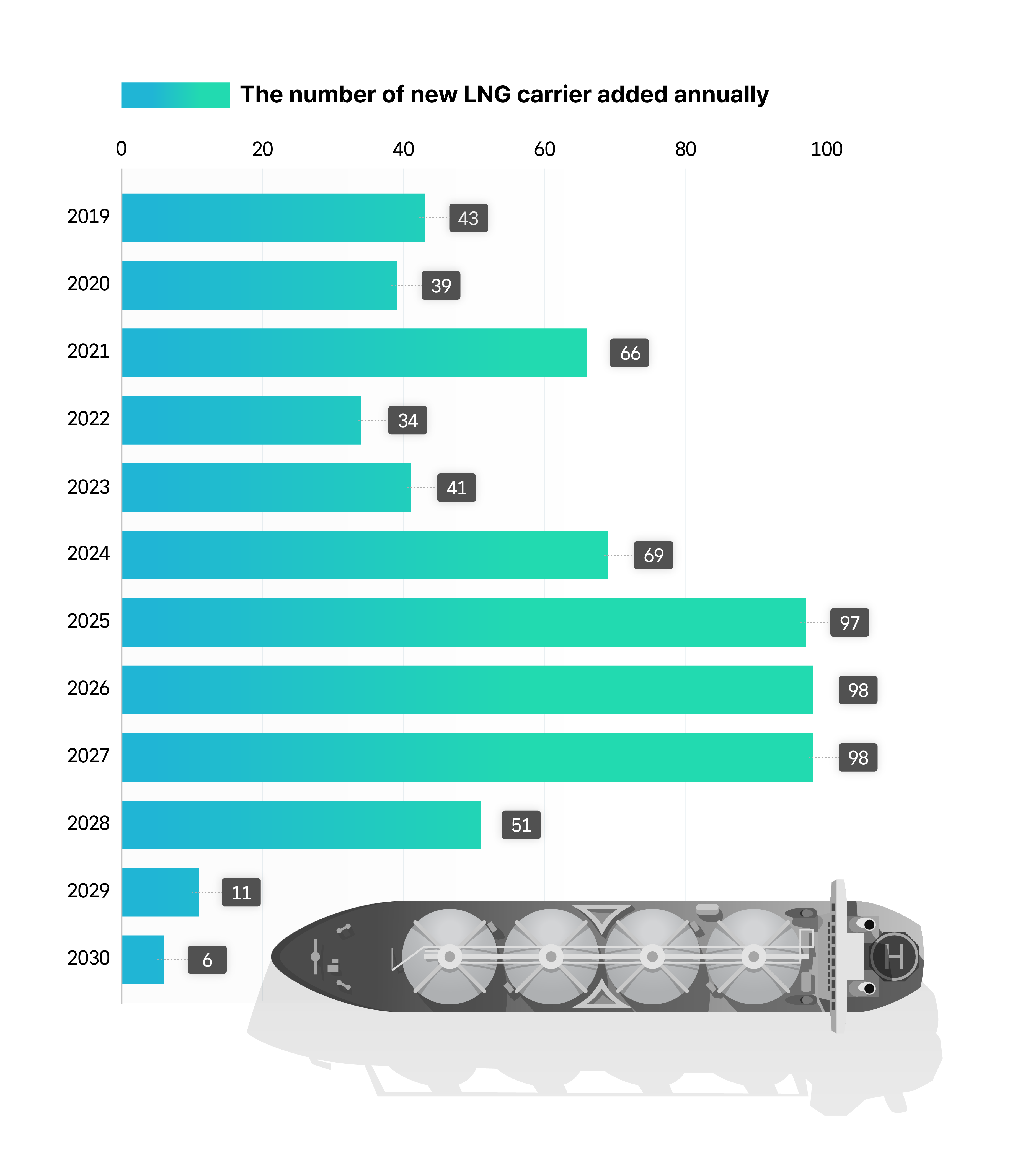

Figure 1: Number of LNG carriers to be delivered annually based on outstanding orders as of July 22, 2025

Data source: Clarkson

According to Clarkson Research, 303 LNG carriers are currently under construction worldwide. Of these, 98 are scheduled for delivery in 2026, and another 98 in 2027—the fastest pace of supply growth in the industry’s history. Such rapid additions to the fleet will likely drive freight rates further down and put increasing pressure on shipping operators.

There are only 209 legacy steam turbine LNG carriers that could potentially create room for new demand. Even the potential phase-out of these carriers is unlikely to offset the wave of new ships. In this oversupplied environment, newer vessels intensify competition, while older ones lose operating opportunities.

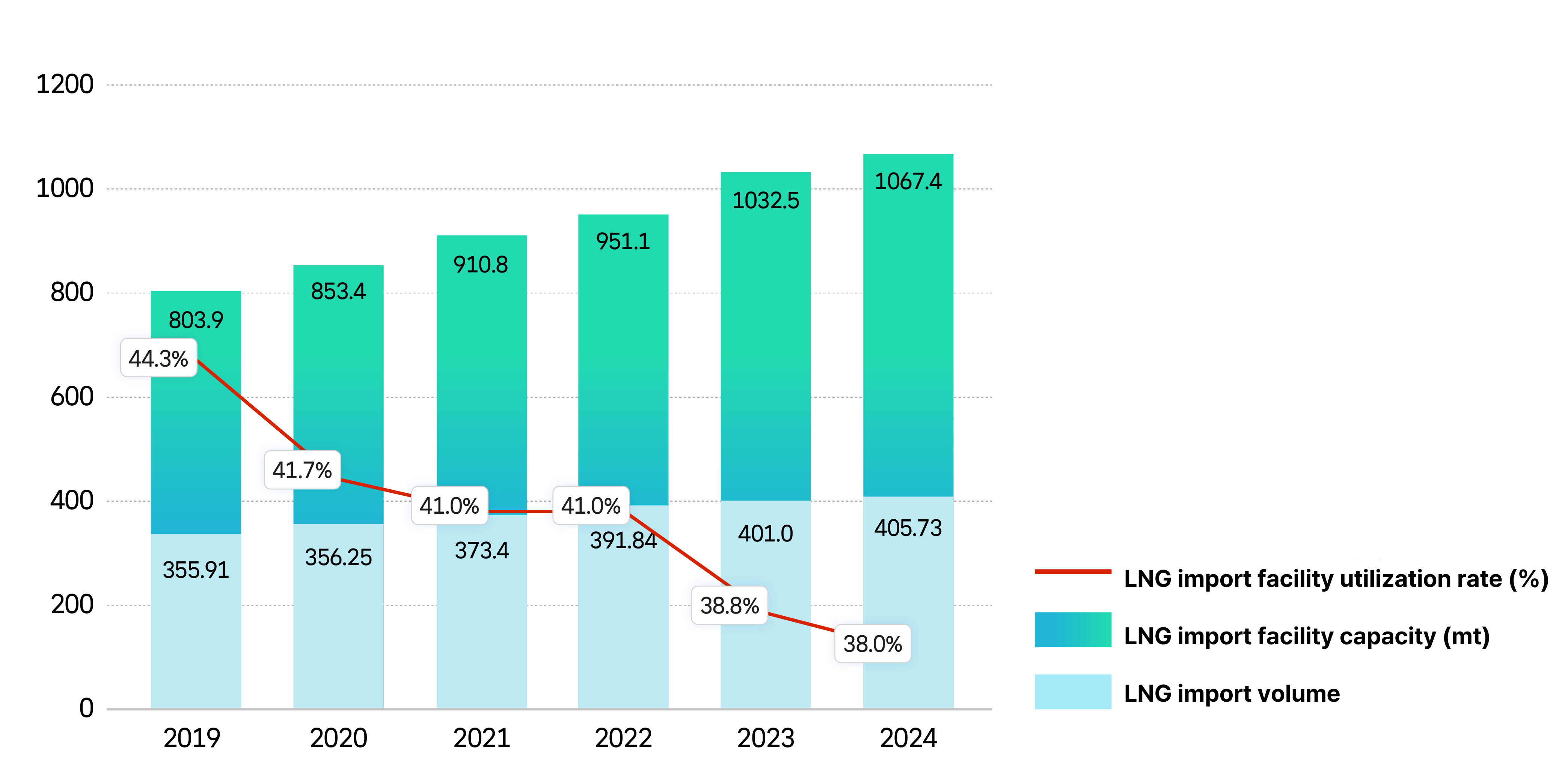

The LNG oversupply is also reflected in LNG import terminal utilization. Global average utilization dropped from 44% in 2019 to 38% in 2024. This decline is largely due to the continued construction of import facilities despite waning demand.

Figure 2: LNG imports and facility indicators

Data source: Kpler

This trend is already having direct consequences for Korean shipbuilders. Most of the LNG carriers ordered between 2021 and 2022 are scheduled for delivery between 2025 and 2027, but fears are rising over a sharp drop-off in new orders beyond that. This so-called “order cliff” could strain the sector’s financial stability. Industry voices are urging a diversification of order portfolios, including a strategic pivot toward eco-friendly vessel segments.

“Korean shipbuilders must reassess their overreliance on LNG carrier orders and start considering strategic shifts toward alternative vessel types and green shipping,” said Yang Jong-seo, senior researcher at the Korea Eximbank Overseas Economic Research Institute, in a media interview.

Some analysts note that the current LNG shipping market crisis mirrors the collapse of the oil tanker market following the oil shock of the 1980s. Back then, an overestimation of future demand led to excessive vessel orders, resulting in market saturation and a downturn that lasted for years. Similarly, today’s crisis is increasingly viewed not as a cyclical slump but as a structural shift tied to the global rise of renewable energy and a fundamental transformation of the energy system. Recovery may take a long time—if it happens at all—as a new market order takes hold. Considering this shift, experts are calling on public financial institutions to adopt more selective and strategic approaches in their support mechanisms.

Rachel Eun-bi Shin, Energy Supply Chain Researcher at SFOC, stated, “Even if older LNG carriers are gradually phased out, the market entry of newly ordered vessels is unavoidable. LNG is increasingly losing out to renewables in terms of competitiveness, and the era of fossil fuel carriers is drawing to a close.” She warned, “even if we see short-term market adjustments, the shipbuilding industry must avoid misjudging the situation in a way that leads to further oversupply of LNG carriers.”

Dongjae Oh, Head of Gas Team at SFOC, emphasized, “In emerging sectors like offshore wind installation vessels, global players are already competing to secure early market dominance. Rather than waiting to provide financing for economically uncertain projects like Mozambique LNG amid a downturn, Korea must act quickly to secure the next growth opportunity for its shipbuilding industry.”

ENDS.

Solutions for Our Climate (SFOC) is an independent nonprofit organization that works to accelerate global greenhouse gas emissions reduction and energy transition. SFOC leverages research, litigation, community organizing, and strategic communications to deliver practical climate solutions and build movements for change.

For media inquiries, please reach out to Antonette Tagnipez, Communications Officer, at antonette.tagnipez@forourclimate.org.

Share this insights

![[Brief] South Korea’s international public finance continues to block a just energy transition](https://content.sfoc.tapahalab.com/images/research/RC5Kime.jpg)

![[토론회] 한국형 녹색분류체계(K-Taxonomy), 무엇이 녹색경제활동인가](https://content.sfoc.tapahalab.com/images/research/bn8jdme.jpg)

![[이슈 브리프] 탄소포집, 이용 및 저장기술(CCUS) 현황과 문제점](https://content.sfoc.tapahalab.com/images/research/SWESdme.jpg)