In This Edition:

Continued standoffs in the Strait of Hormuz expose the risks and wide-reaching impacts of Asia’s deeply entrenched dependency on oil and gas.

Countries across East and Southeast Asia struggle to break the LNG dependency loop under pressure to ensure energy security amid intensifying geopolitical shocks

Asian supply chains brace for impact as the EU’s Carbon Border Adjustment Mechanism puts a price tag on embedded emissions from imported steel, cement, aluminum and the like.

As the impacts of climate change intensify across the globe, growing pressure to phase out greenhouse gas (GHG) emitting fossil fuels is coming from multiple angles. Oil and gas have long been more than energy resources — they are geopolitical assets, shaping the foreign policy, alliances, and economic leverage of nations throughout modern history.

The current crisis in the Strait of Hormuz, a major maritime chokepoint through which around 20% of the world’s oil supply and significant volumes of LNG transit on a daily basis, is a prime example. On February 28, 2026, US-Israel attacks on Iran triggered the effective closure of the strait, immediately and significantly destabilizing global oil and gas trade. In the weeks since, the two countries’ continued threats to Iran’s energy infrastructure, retaliatory attacks in neighboring countries and the US’ current reverse blockade continue to prolong what experts have called “the worst global energy supply disruption in history”, costing thousands of civilian lives in the process.

These developments have not occurred in a vacuum. For Asia, the destination of more than 80% of oil and LNG passing through the Strait of Hormuz, the conflict has once again put the long-known inherent risks of fossil fuel dependency back into stark focus, forcing countries across the region to reevaluate their approaches to energy security.

If the current energy crisis sits in one hand, the other is occupied by a ticking time bomb putting a long overdue price tag on carbon emissions across Asian supply chains. The European Union’s Carbon Border Adjustment Mechanism (CBAM), which came into effect earlier this year, is a carbon tariff system aimed to prevent carbon leakage and put a fair price on production in carbon-intensive industries like steel, cement and aluminum entering the EU. For Asian exporters, the implications are grave, especially with a proposed extension of the CBAM’s regulatory scope to include downstream products like auto parts, construction equipment and heavy machinery on the table.

Between a rock and a hard place, Asia is struggling to rapidly regain some semblance of energy security while attempting to escape an outdated fossil fuel model increasingly challenged by emerging global regulatory mechanisms like the CBAM, designed to price out dirty industries and energy production. In this edition of the ACS newsletter, we dive into how countries across the region are navigating these murky waters, unpacking the factors which could determine Asia’s ability to realize a successful clean energy future.

The Hormuz Blockade: Asia’s Wake-Up Call

In the immediate aftermath of the February 28 attacks, traffic through the Strait of Hormuz collapsed, dropping from 77 crossings to just 4 by March 3. War risk insurance premiums for crude oil tankers and LNG carriers skyrocketed, further deterring ships needing to berth and take on cargo. In the weeks since, continued tensions have meant increasingly volatile fuel prices and shortages of key raw materials like naphtha (used to make plastics), graphite and sulfur (battery production) and helium (heavily used in semiconductor manufacturing).

For Asia, the biggest importer of oil, gas and related materials passing through the Strait of Hormuz, the current crisis has forced regional governments to face the reality of fossil fuel dependency head-on. It follows a long-standing pattern which has emerged from the 1973 oil embargo to Russia’s 2022 invasion of Ukraine, highlighting a persistent structural vulnerability where geopolitical instability leads to immediate, punishing costs for import-dependent Asian economies.

Asia’s Fossil Fuel Reckoning

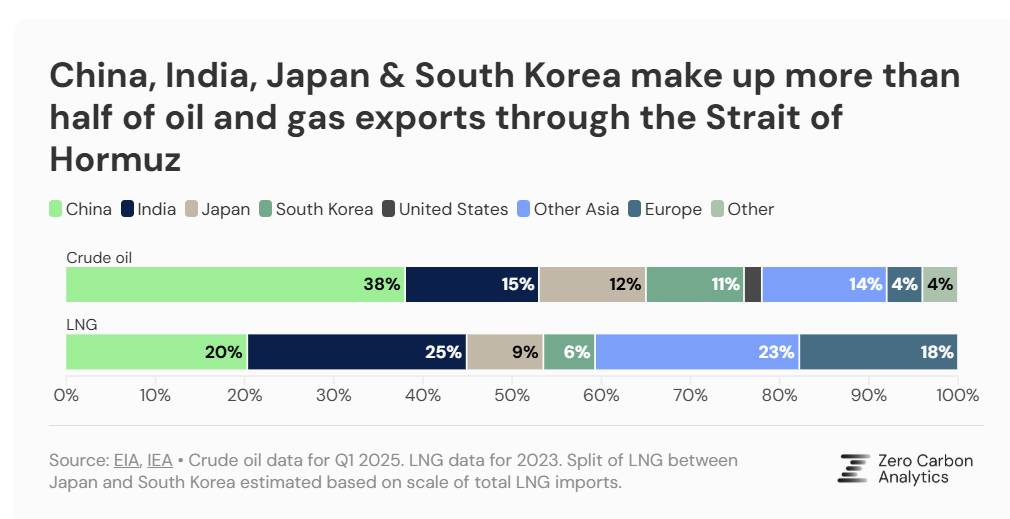

In 2024, 84% of oil and 83% of LNG exports passing through the Strait of Hormuz were destined for Asian markets. Recent numbers indicate China, India, Japan and South Korea alone account for 75% of oil and 59% of LNG traffic passing through the strait.

SFOC’s latest analysis documents a dramatic economic shock in the intermediate aftermath of the first Hormuz blockade: WTI crude prices climbed to US $112, while Asian LNG benchmarks soared by 69%. This volatility battered regional markets, causing the Korea Composite Stock Price Index (KOSPI) to plunge by over 12% and forcing both the Korean won and Japanese yen to hit multi-month lows as the rising cost of energy imports weighed on currency stability.

Across the region, governments are implementing short-term measures to cushion the blow for citizens and industries. Japan has officially begun tapping into strategic oil reserves, Indonesia is expanding fuel subsidies and accelerating biofuel expansion and China is making moves to block fuel exports to protect its domestic supply, while Thailand, Vietnam and the Philippines look to Russian oil. On April 13, the South Korean government lifted limits on coal-fired power generation capacity and raised nuclear power plant utilization rates, emergency moves some argue dovetail with the country’s recent climate commitments.

Across Southeast Asia, skyrocketing fuel costs have priced transport workers and fishers out of their livelihoods, leading to docked tourist boats, grounded fishing fleets, and mass strikes by transit drivers. To mitigate the "imminent danger" to energy security, regional leaders have declared states of emergency and implemented radical conservation strategies, including shortened work weeks, work-from-home mandates, and even the suspension of school meal programs to divert funds toward oil procurement. As fuel shortages threaten to inflate food prices and further destabilize supply chains, Asian countries are aggressively seeking to diversify their import sources, hoping to prevent a total economic collapse while the conflict persists.

The Downsides of Dependency: Japan and South Korea

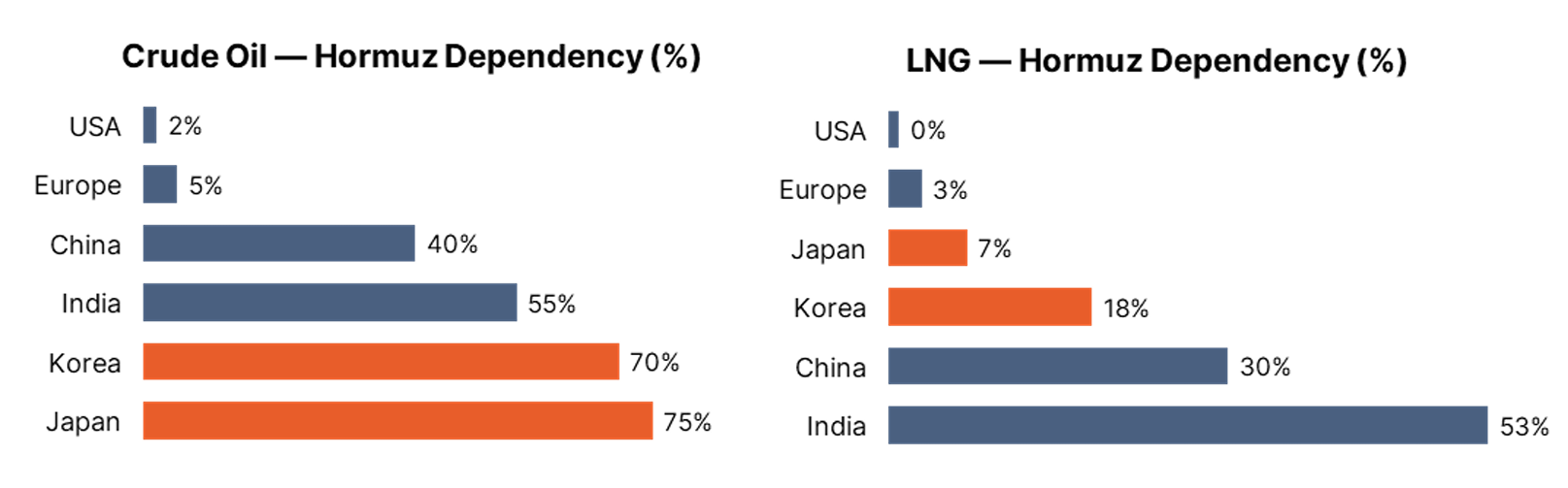

For Japan and South Korea in particular, heavy reliance on fossil fuel imports from this geopolitically sensitive region means disproportionate exposure to price shocks emerging from the current crisis, throwing a wrench into LNG-dominated energy security strategies. South Korea funnels 70% of its crude oil and 18% of its LNG imports through the two-mile wide Strait of Hormuz, with Japan’s slightly more diversified LNG import portfolio leaving its rate of dependency at a lower 7%.

Despite its resilience-building efforts, new models predict Japan, described as “the most Hormuz-dependent major economy,” still faces the greatest direct risks of supply disruption in the strait, with more than 90% of its crude oil imports originating in the area. Korea follows closely behind, its LNG carrier shipbuilding dominance becoming a liability in the face of growing stranded asset risks.

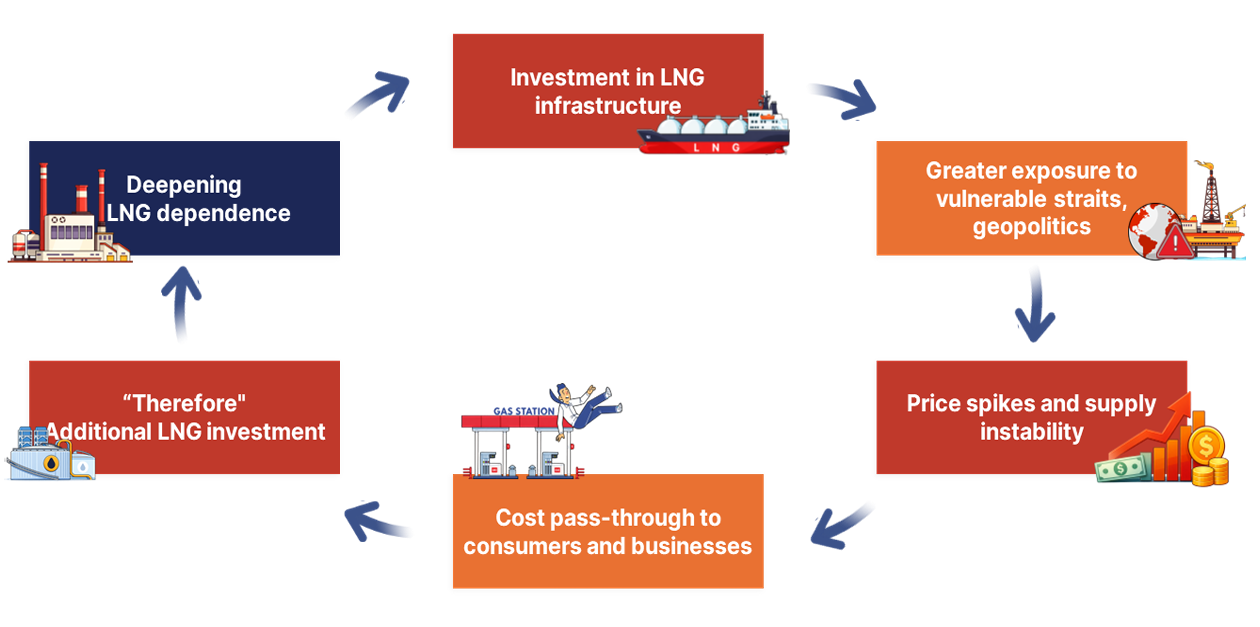

Asia’s LNG Dependency Loop: Lessons Not Learned

For heavily LNG import-dependent countries, like many across Asia, supplier diversification has long been the modus operandi when faced with sudden geopolitical shocks. South Korea and Japan, for example, are ramping up LNG imports from Qatar, Australia, Southeast Asia and the United States, attempting to circumvent the Hormuz fallout.

These are not new trends. The 2022 Russian invasion of Ukraine saw a similar kneejerk reaction from major Asian economies: despite little to no change in demand, Korea’s LNG spending doubled to US $50 million in just a year, with Japan’s LNG bill increasing by 65.2% from its 2021 numbers. In the face of another geopolitical shock, these patterns are repeating themselves. Long-term supply agreements in Japan like JERA's reported 27-year deal with QatarEnergy and Mitsui's continued interest in the North Field expansion have been positioned as energy security strategies, while Korean shipyards brace for increased LNG carrier orders as customers scramble to spread out their purchases in less volatile regions. In Korea, LNG carrier buildout has been heavily backed by public financial institutions, including KEXIM that has committed $44.1 billion in guarantees and loans for LNG carrier shipbuilding in the past decade. Geopolitical shocks then generate fresh pressure on these institutions to expand that underwriting further, even as the underlying market shows structural oversupply.

What emerges is a self-reinforcing cycle where continued buildout of LNG infrastructure heightens susceptibility to geopolitical disruptions and other related risks, which, ironically, is then used to rationalize additional LNG investment in the name of energy security. Diversification merely reinforces existing dependency, bringing only temporary relief and potential short-term gains while the fate of countries’ entire energy systems hangs in the balance.

Paradoxically, the positioning of LNG as the saving grace of a collapsing fossil fuel-based economy, rather than increasing ever-elusive energy security, inadvertently undermines it. The impacts of the Hormuz blockade will not be limited to Asia; disruptions anywhere in the LNG supply chain will be felt everywhere. Spreading out the risks of LNG dependency will not eliminate them.

A Bill Comes Due: The EU Carbon Border Adjustment Mechanism (CBAM)

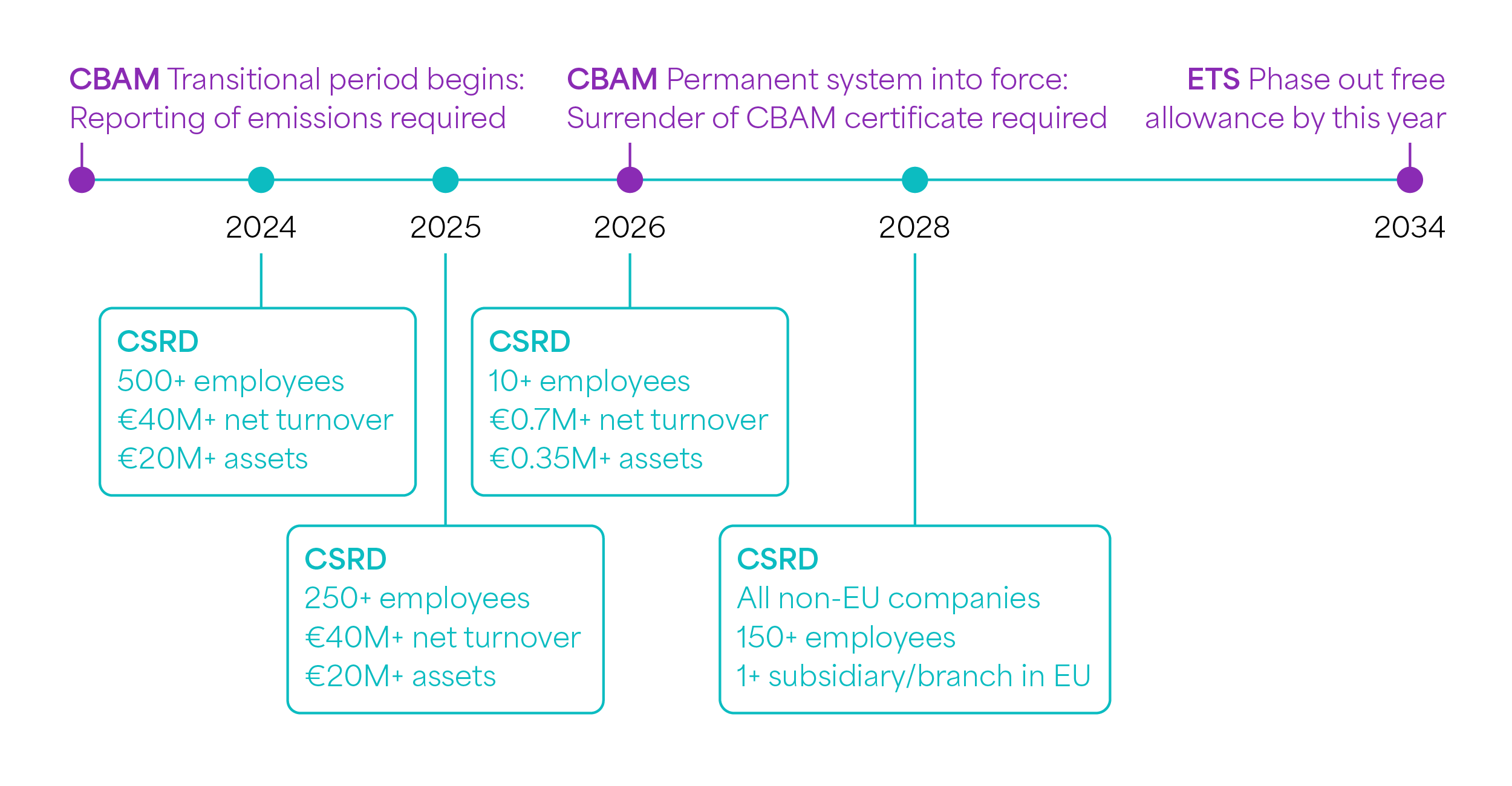

Amid supply chain disruptions and potential energy shortages originating out of the Hormuz crisis, Asia’s industries must now navigate an emerging trend of strengthening global carbon regulations like the EU’s Carbon Border Adjustment Mechanism (CBAM). Its transitional phase began in October 2023, allowing both EU and non-EU producers, importers and authorities to gradually begin reporting their supply chain emissions across industrial sectors like iron and steel production, electricity and hydrogen.

The CBAM principle, on paper, is simple. It seeks to make sure carbon-intensive imports are subject to the same carbon pricing system as EU-made products. The ultimate goal is to prevent carbon leakage, where strengthening climate regulations for industries in one country or region ends up pushing industries and their emissions to regions with much weaker climate policies, essentially cancelling out any real GHG reduction.

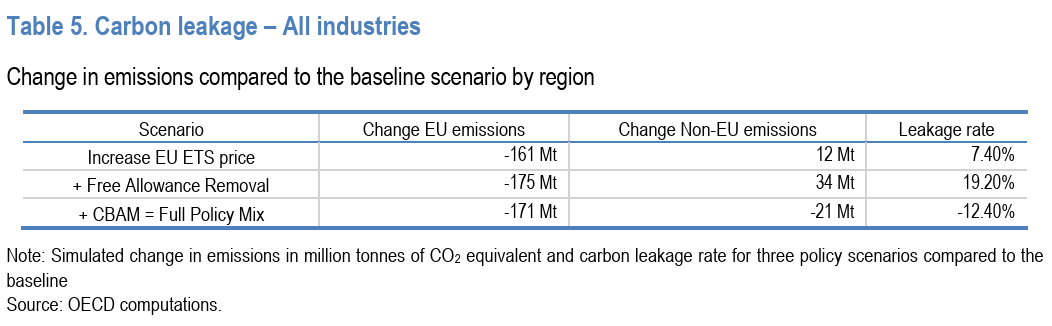

At present, the CBAM applies to 303 products across six high GHG-emitting sectors: cement, iron and steel, aluminum, electricity, hydrogen and fertilizers – but the list doesn’t stop there. Starting from 2028, the EU plans to expand CBAM’s scope to include downstream outputs, which could have significant implications for industries like manufacturing, automotive production and construction, where carbon emissions are deeply embedded across existing supply chains. A recent OECD Working Paper predicts that combined with the removal of free allowances and increased carbon prices under the EU’s existing Emissions Trading System (ETS), CBAM implementation could result in a negative carbon leakage rate, reducing global emissions by around 0.54%, just over 190Mt of CO2e.

The EU published the first-quarter CBAM certificate price on April 7, available for companies to purchase at the rate of €75.36 ($89.64) per tCO2e.

What’s at Stake for Asia

59% of the EU’s imported steel originates in Asia, with countries like Türkiye, South Korea, India and Vietnam topping the supplier list. In Japan, South Korea and China, steel produced from carbon-intensive, coal-based blast furnaces will face levies matching their embedded emissions, with potential added costs running up to 20-35% of the original export price.

Aluminum smelters in Indonesia running on coal-fired grid electricity face similar exposure, while Indian steel, aluminum and cement exporters, already navigating thin margins, are watching Brussels closely.

The intensity of the fallout from CBAM’s full implementation will depend heavily on domestic carbon pricing across Asia, which recent studies say could significantly decrease the threat of higher export fees at the EU border. Under CBAM, importers that “pay” the price for – or clean up – their emissions in their home countries can claim a reduction in the number of CBAM certificates they need to purchase. The maturity of Asian carbon pricing systems, however, vary widely across the region: Japan and South Korea’s ETS cover around 50% and 80% of national emissions respectively, while similar systems and instruments in countries like Indonesia, Vietnam and the Philippines are still in the nascent stages of development.

CBAM in Focus: Japan and South Korea

According to a recent model from think tank Sandbag, Japan and South Korea are set to face the highest CBAM fees upon full implementation. In the case of South Korea, estimates suggest that steel exporters will incur approximately KRW 127 billion (around EUR 85 million) in CBAM-related carbon costs in 2026, potentially exceeding KRW 1.8 trillion (EUR 1.2 billion) annually by the early 2030s. For Japan, that figure could go up to ¥45 billion (EUR 285 million), just under 1% of the value of their traded goods.

The ripple effects of CBAM implementation will extend far beyond the directly regulated sectors, affecting supply chains across the automotive, electronics manufacturing, plastics and even agricultural and food processing industries. It is also worth noting that CBAM will not remain the only mechanism of its kind for much longer. A similar regulation is under development in the UK, while Canada is exploring carbon border adjustments and proposals circulate in the US Congress.

In essence, CBAM provides a strong incentive for Asian governments to ensure their emissions trading systems (ETS) effectively accelerate decarbonization across heavy-emitting industries. As coverage increases, producers who adapt in the early and can credibly demonstrate low-carbon production will find themselves advantaged not just in the European market, but in the emerging architecture of a carbon-priced global economy that is soon to be a reality.

This process has already begun. Tier 1 and Tier 2 suppliers across the region are starting to receive questionnaires from European buyers asking them to account for Scope 1 and Scope 2 emissions. For many, the administrative burden alone is unfamiliar territory. Countries such as India are adopting procurement systems based on carbon intensity, while ASEAN nations are preparing emissions trading schemes that will price products according to their actual emissions. South Korea is also shifting toward physically grounded decarbonization and renewable energy expansion strategies in response to international pressures. This includes initiatives like the construction of RE100 industrial complexes and the “sunlight income village” program, a profit-sharing model that sees local residents invest in solar power buildout in exchange for a portion of the revenue from power generated on to the national electricity grid.

How Asia is Bracing for Impact

Taken together, the Hormuz disruption and the CBAM trajectory describe a single, converging pressure: the fossil fuel-intensive development model that built Asia's industrial strength is becoming simultaneously more fragile, structurally risky and more expensive. The pains and groans of the transition, often cited as a reason for delay, are starting to pale in comparison to the compounding costs of staying put. As countries attempt to navigate dual crises of growing energy demand and increased vulnerability to geopolitical and economic shocks like the ones we see now, decisions made in the near future will make or break Asia’s ability to escape the fossil fuel trap.

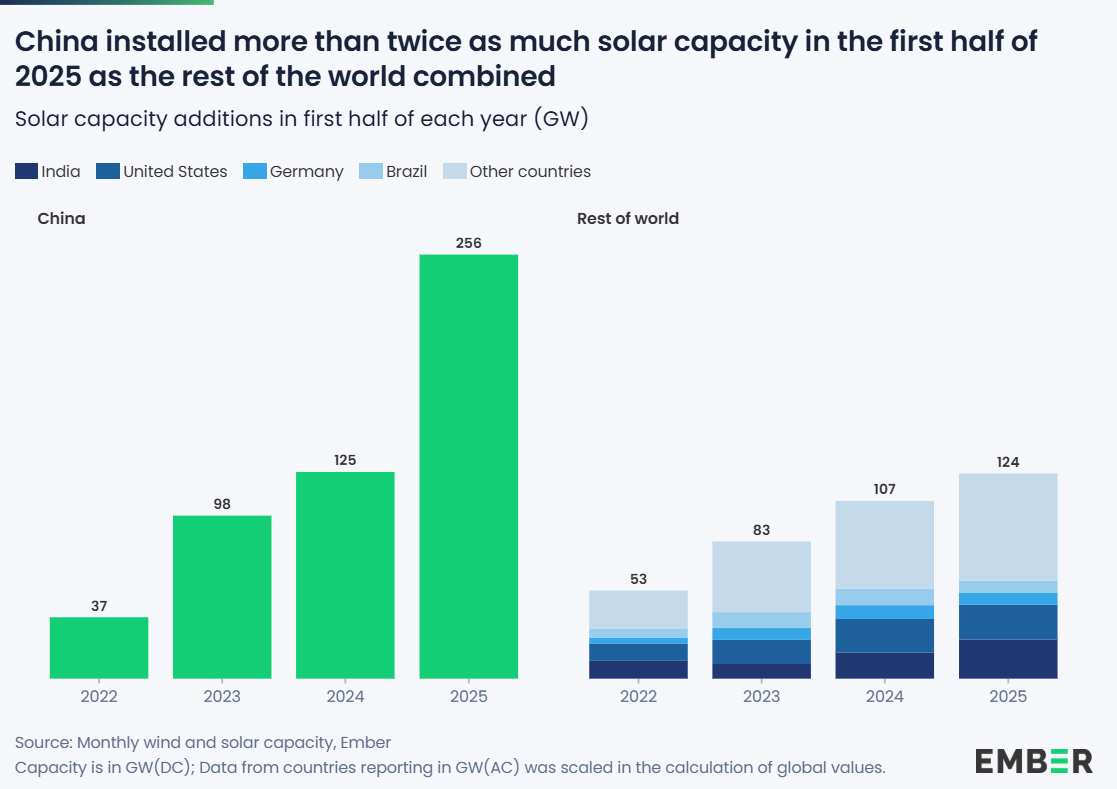

In technical terms, Asia has the scale, the engineering capacity, and in several countries, the political will to move decisively and navigate towards a clean energy transition. China installed 256 GW of solar capacity in 2025 alone, more than the rest of the world combined. South Korea is speeding up photovoltaic energy projects by easing solar siting rules to cut permitting delays. Japan, long cautious, has begun to accelerate offshore wind permitting in ways that would have seemed bureaucratically impossible years ago.

At the same time, these moves to reduce dependency on fossil fuels like LNG must be supported by measures which make decarbonizing Asia’s hard-to-abate industries the most financially viable course of action. This means ensuring carbon pricing systems function as designed: setting clear caps on emissions, phasing out carbon offsetting and shifting from loophole-filled free allocation models to auctioning models which send real price signals to the market.

Asia’s Choice

The Hormuz blockade and the EU Carbon Border Adjustment Mechanism (CBAM) are just two of many emerging converging pressures shaking up Asia’s energy status quo. What they signal, somewhat painfully, is urgency. In both cases, Asia, perhaps more than any other part of the world, has borne and will continue to bear the brunt of the fallout. The strait may reopen, but the carbon borders measures are set to evolve rather than disappear, and if history is anything to go by, the Hormuz crisis will not be the last of its kind. At this juncture, Asia has choices to make, and half-measures will no longer work.

Asia, the continent that shaped the 20th century industrial economy, brings together scale, industrial capacity, and growing expertise, but its ability to lead the global clean energy transition will depend on closing persistent gaps in finance, policy frameworks, institutional capacity, and the technical know-how across the region. While several countries have moved forward rapidly, others, particularly least developed economies, face far deeper structural constraints. In the end, the path towards decarbonizing Asia’s industries and economies will be carved not by those who are best poised to merely react, but by those with the courage and wisdom to move first.