The global automotive industry is at a turning point. Automakers face rising material costs, uneven demand across regions, and an increasingly complex regulatory environment. At the same time, investors are demanding stronger climate commitments and credible transition plans.

For Hyundai Motor Company, Asia’s second-largest automaker, this moment is especially urgent. The recent federal raid on Hyundai and LG Energy Solution’s joint EV battery plant in Georgia brought unexpected attention to the company’s US operations, not only on its labor practices but also on its broader role in America’s EV transition. As Hyundai invests billions to expand production in one of its most important markets, it faces growing pressure to match its rapid operational expansion with equally credible climate and sustainability commitments.

Hyundai has taken meaningful steps to prepare for the low-carbon transition. Its 2025 Sustainability Report aligns with global frameworks such as TCFD, SASB, and ESRS, includes quantified physical-risk scenario outputs, and pledges carbon neutrality by 2045. It has set electrification targets of 100% sales in Europe by 2035 and in major markets by 2040, with a $87 billion (KRW 120.5 trillion) investment plan through 2033 in electrification, software, and sustainability initiatives. These are strong top-line ambitions and signal growing integration of climate considerations into corporate strategy.

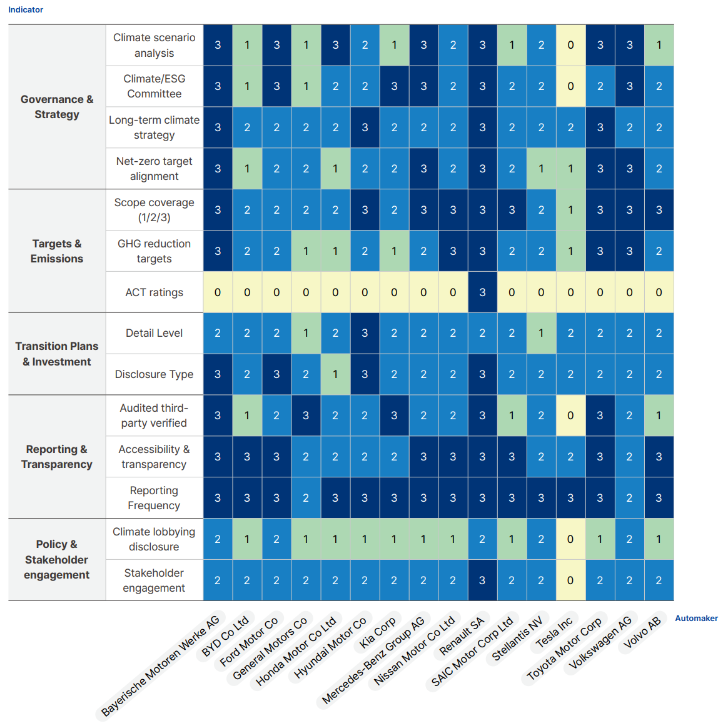

Figure 1. Climate disclosure score by automaker (Source: Empower, Solutions for Our Climate (SFOC))

However, ambition alone is not enough. Hyundai’s disclosures still show significant gaps compared with the best global practice. Its Scope 3 reporting covers broad categories such as purchased goods and use of sold vehicles but lacks the material- or supplier-level granularity that investors need to assess supply-chain risk. Third-party assurance is limited mainly to domestic Scope 1–2 data, and methodological transparency on baseline years and scenario assumptions remains incomplete.

Most notably, Hyundai’s 2045 net-zero pledge has not been validated by the Science Based Targets initiative (SBTi), the most widely recognized benchmark for credible emissions targets. Many automotive companies — including Ford, GM, BMW, and Renault — have secured SBTi validation. In some markets, this is now more than a reputational issue. The UK ties certain EV subsidies to SBTi-approved targets, and the EU’s regulatory landscape is moving toward requiring verifiable data for everything from lifecycle battery emissions to supply-chain due diligence. Without validation, Hyundai risks being seen as a laggard at a time when credibility is becoming a commercial advantage.

Investors are also looking for near-term milestones and clear capital-allocation signals. Hyundai has set interim reduction targets for Scope 1–2 and downstream use-phase emissions but provides few checkpoints for 2030 and has adjusted some base years, creating uncertainty about progress. Its KRW 120.5 trillion investment plan is significant but does not disclose the split between EV and internal-combustion-engine (ICE) programs — a key data point for investors seeking to understand whether capital spending is aligned with transition goals.

According to a report by Solutions for Our Climate (SFOC), Hyundai’s scenario and risk analysis shows progress — including estimates of potential facility losses under IPCC climate pathways and projected carbon compliance costs under Europe’s CBAM — but stops short of fully linking these risks to cash flow, profitability, or asset-stranding exposure. In contrast, leading European automakers are publishing detailed analyses that allow investors to model financial resilience under 1.5°C and 2°C scenarios.

All of this is happening as global regulations are tightening. The EU Corporate Sustainability Reporting Directive (CSRD), ISSB standards, and new supply-chain due diligence laws are converging toward mandatory, comparable, and investor-grade climate disclosures. In parallel, policies like California’s 2035 zero-emission sales mandate are accelerating the timeline for ICE phase-out. Automakers that fail to provide credible roadmaps risk financing challenges and shrinking access to climate-conscious capital — while those that lead stand to benefit from lower cost of capital, better access to green bonds and sustainability-linked loans, and stronger market positioning.

Hyundai’s Executive Chair, Euisun Chung, underscored the company’s ambition earlier this year when he announced a $21 billion U.S. investment plan amid tariff uncertainty — an important signal to investors that Hyundai is betting big on its future. Aligning this scale of investment with a clearly defined, SBTi-validated climate strategy would send an equally strong signal that Hyundai intends to lead not just in EV sales, but in the credibility of its transition plan.

Hyundai has already proven that it can compete technologically with the best — the IONIQ 5 and IONIQ 6 have won global awards and expanded the company’s EV market share. Now the task is to match product leadership with disclosure and strategy leadership. By validating its targets, expanding Scope 3 reporting, integrating financial scenario modeling, and aligning its lobbying with its climate commitments, Hyundai can reassure investors, meet rising regulatory standards, and secure its place among the global frontrunners driving the industry’s shift to a low-carbon future.

Related insights

Advancing the Transition Away from Fossil Fuels

Key Outcomes from Santa Marta

2026-05-29

Green Steel Standard Development in East Asia

Green Steel Standards Blog Series #2

2026-05-13

Miles to be Heard by Those Who Never Had to Live Downstream: UBS's Exposure to Thai Energy Projects Flagged at the AGM

Thai villager carried years of struggle to UBS's doorstep.

2026-05-11

Is 'Green Steel' Actually Green? Why Standards Matter

Green Steel Standards Blog Series #1

2026-04-30

Explained: The Public Finance Mechanisms Keeping the LNG Carrier Industry Afloat

How Government Funds are De-risking LNGC Expansion

2026-04-02

Explained: How Private Banks are Enabling LNG Carrier Expansion

How finance, not demand, is keeping the LNG carrier industry afloat

2026-03-09

Financing the Climate Crisis: South Korea’s Global Fossil Fuel Footprint

The Role of Public Financing Institutions in the Age of Climate Change

2025-06-04

What South Korea’s Next President Must Do to Address the Climate Crisis

SFOC’s 10 Climate Solutions

2025-05-02

Green Promises, Dirty Money: The Silent Support Behind KEPCO’s Fossil Expansion

KEPCO’s Investors and Underwriters: Ignoring the Warnings, Enabling the Problem

2025-04-10